Dhaka, Bangladesh (BBN)- Bangladesh’s banking sector has plunged into its weakest capital position in history, with capital adequacy levels falling far below international standards and trailing behind all neighbouring South Asian countries.

The development has raised alarm over the resilience of the country’s financial system, according to the Bangladesh Bank (BB)’s latest Financial Stability Report (FSR) 2024.

CRAR Falls to 3.08 Per cent

The capital-to-risk-weighted-asset ratio (CRAR) — a key measure of banks’ financial health — fell to 3.08 per cent at the end of December 2024, down drastically from 11.64 per cent a year earlier.

The fall of over eight percentage points in a single year underscores the severe pressure banks are facing due to a combination of rising non-performing loans (NPLs) and weak capital buffers.

The central bank report pointed out that state-owned commercial banks (SoCBs), specialized development banks (SDBs), and Islamic private commercial banks (PCBs) were primarily responsible for pulling down the industry average, given their fragile balance sheets.

“The banking sector faced heightened stress in 2024, particularly regarding capital adequacy,” the BB said in its FSR.

NPLs Surge to Record BDT 3.45 Trillion

The crisis stems largely from the rapid growth of NPLs. Classified loans in the banking system surged by more than BDT 2.0 trillion year-on-year, hitting a record BDT 3.45 trillion by December 2024. That means nearly one in every five taka in bank lending has now turned non-performing, as NPLs accounted for 20.20 per cent of the total BDT 17.11 trillion in loans disbursed by all scheduled banks.

This surge in default loans forced banks to set aside larger amounts from their capital as provisioning against loan losses, severely eroding their capacity to maintain the required capital adequacy.

“Higher non-performing loans have pushed down the CRAR of Bangladesh’s banking system to the lowest level among neighbouring countries as of end-December 2024,” said Mohammad Shahriar Siddiqui, acting spokesperson and a director of the central bank.

He added that banks have been instructed to expedite loan recovery drives to shore up their financial health.

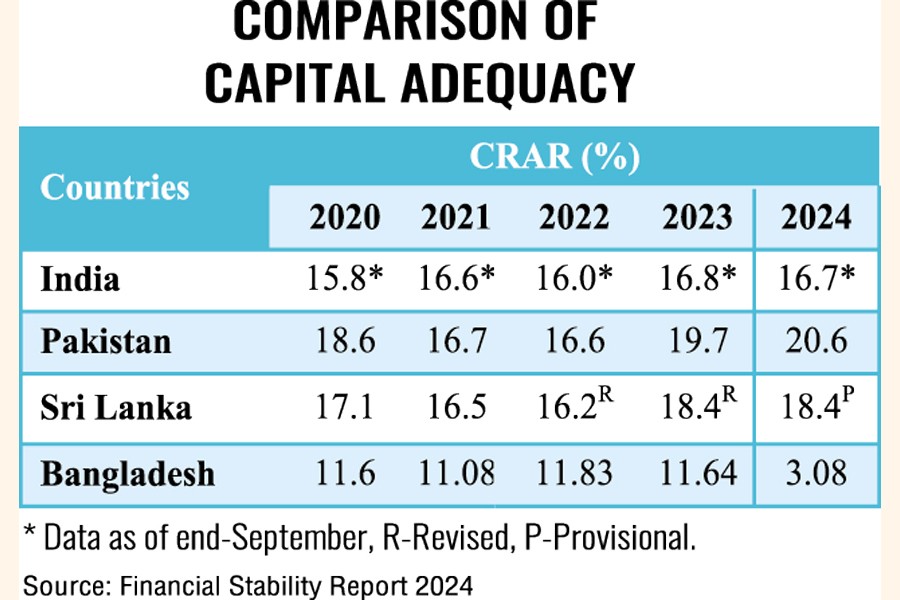

Lowest in South Asia

The FSR compared Bangladesh’s position with other SAARC nations, exposing the scale of the weakness. Pakistan maintained the highest CRAR in the region at 20.6 per cent in 2024, followed by Sri Lanka at 18.4 per cent and India at 16.7 per cent (as of September 2024). Bangladesh trailed far behind at just 3.08 per cent, raising questions about its compliance with global regulatory standards.

Basel-III Framework under Strain

Bangladesh adopted the Basel-III framework in 2015, requiring banks to maintain a minimum CRAR of 10 percent, along with a 2.5 per cent capital conservation buffer (CCB) in the form of common equity tier-1 (CET-1) capital.

The framework, developed by the Basel Committee on Banking Supervision in the aftermath of the 2008 global financial crisis, aims to strengthen banks’ resilience to shocks and improve liquidity management.

However, the present capital position of Bangladeshi banks shows a wide gap between regulatory requirements and actual performance. With CRAR now at 3.08 percent, most banks are far short of the regulatory threshold, highlighting systemic vulnerabilities.

Implications for Financial Stability

Analysts warn that prolonged weakness in capital adequacy could undermine confidence in the banking sector, restrict credit growth to the private sector, and weigh on overall economic performance.

“The significant deterioration of capital adequacy in SoCBs, Islamic PCBs, and SDBs highlights the need for intensified supervision and targeted measures,” the FSR observed. “Strengthening their capital base is critical to bolstering individual resilience as well as the stability of the overall financial system.”

BBN/SSR/AD