Frankfurt, Germany (BBN)-There are “no limits” to how far central banks can ease monetary policy.

That’s a recent declaration of both European Central Bank President Mario Draghi and Bank of Japan Governor Haruhiko Kuroda, who have joined their counterparts in Denmark of Sweden and Switzerland in embracing interest rates of less than zero, reports Bloomberg.

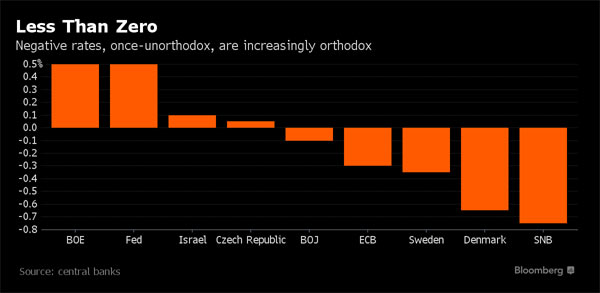

In September 2014, when the ECB’s deposit rate was minus 0.2 per cent, Draghi was saying “now we are at the lower bound.”

As recently as December, Kuroda said “we don’t think we should institute” negative rates.

The rethink is global, even in places where rates are still positive.

Bank of England Governor Mark Carney conceded in November that his benchmark could fall below the current 0.5 percent if needed, while Federal Reserve Vice Chair Stanley Fischer said last week that negative rates were “working more than I can say that I expected in 2012.”

Citigroup Inc economist Willem Buiter says even China could shift below zero next year.

The worry had been that probing below zero risked hurting the profitability of lenders, forcing them to pass on the cost to borrowers.

Other fears included bank and currency runs, the hoarding of cash or gridlocked money markets.

Rather than spurring lending and spending as intended, subzero rates would become more a problem than solution.

Such a concern could still flare up a new given the recent selloff in global bank stocks and fretting over financial titans such as Deutsche Bank AG.

So in this brave new world, how much lower can rates now go?

According to an analysis published late on Tuesday by economists at JPMorgan Chase & Co, way, way lower.

Having studied the lack of fallout in Switzerland, where the benchmark rate is minus 0.75 per cent, Malcolm Barr and Bruce Kasman reckon the trick lies in a tiered system as already deployed by the Bank of Japan and in some places of Europe, whereby only a portion of reserves are subjected to negative rates.

On that basis, they estimate if the ECB just focused on reserves equivalent to 2 percent of gross domestic product it could slice the rate it charges on bank deposits to minus 4.5 per cent.

That compares with minus 0.3 percent today and the minus 0.7 percent JPMorgan says it could reach by the middle of this year.

The Bank of Japan’s lower bound on a similar basis may be minus 3.45 percent, while Sweden’s is likely minus 3.27 per cent, the economists said.

Should they also go negative, the Fed could cut to minus 1.3 percent and the Bank of England to minus 2.69 per cent in JPMorgan’s view, reflecting how the ratio of reserves to assets is higher in their economies than elsewhere.

OUT OF AMMUNITION

Concentrating on 25 per cent of reserves would allow the ECB to cut to minus 4.64 percent and the Fed to minus 0.78 per cent.

Making no change to the current regime would allow Draghi to lop to minus 1.36 percent, they said.

Easing the fall is that the JPMorgan economists bet that banks are unlikely to be able to pass on the cost of the policy to borrowers, reducing potential repercussions.

They also see limited pressure on bank profits or for a need to stash cash.

While Barr and Kasman still expect policy makers to tread carefully, such analysis may temper the recent fear of investors that after seven years of interest rates around zero and bumper bond-buying, central banks are now out of ammunition.

Indeed, a fuller embrace of negative rates could “produce significant reductions in market rates,” said the economists.

“It appears to us there is a lot of room for central banks to probe how low rates can go,” they said.

“While there are substantial constraints on policymakers, we believe it would be a mistake to underestimate their capacity to act and innovate.”

BBN/TR/AD