Dhaka, Bangladesh (BBN)- A HSBC research study expects only moderate appreciation of the BDT, with USD-BDT forecast to reach BDT 76 against one US dollar by the end of 2013.

"We feel that the recent downward movement in USD-BDT will continue. The BDT has strengthened on account of strong current account flows, which are expected to continue in 2013," the HSBC research titled 'Asian FX Focus' said.

It also said the capital account still remains a potential point of weakness though. Positive developments are expected in this direction as well.

"For example, the central bank has started to focus on enhancing the short-dated portion of bills/bonds issues, which may attract greater foreign investment than we have seen so far. The authorities are also investing in financial infrastructure, for instance launching an electronic trading window on the central bank's website, which may make it easier for foreign investors to trade the BDT and invest onshore."

The factors like reduced food prices, increased remittance flows' possible upward pressure on asset prices and fuel non-food inflation, the central bank's possible intervention to stem BDT strength and political uncertainty arising from elections, which will likely take place in the first half of Q3 of 2013 might pose a challenge to sustainable appreciation of the BDT.

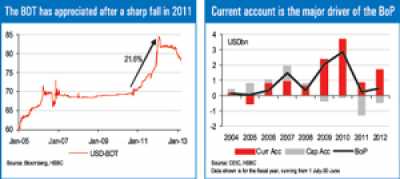

Trade and remittances - the twin engines of BDT strength

The largest driver of the current account is remittances from overseas Bangladeshi workers. This flow is large, given the overall size of the Bangladeshi economy, and is substantial enough to keep the current account in surplus.

The latest data shows these flows remain robust. In the first six months of fiscal year 2013 (July- December 2012), remittances printed growth of nearly 20 percent.

One factor supporting the ongoing rise in remittances is the strength of the economies where most overseas Bangladeshi workers are based. More than 60% of remittance flows come from the Gulf nations. Meanwhile, Asia's growing demand for labour is precipitating a slow shift in the location of workers. Bangladesh is entering into various agreements with Asian economies like Malaysia, Hong Kong and China to supply labour to these economies.

This has seen Asia's share of overseas workers pick up gradually. A recent study by the World Bank1 suggests that the growth of remittances will be stronger during 2013-15, particularly in regions that rely on remittance flows from the Gulf Corporation Council (GCC), the US and Russia.

Asia should also provide relatively strong growth for foreign workers. However, there may be some risks. One concern would be that Asia's economies become less open to the entry of unskilled labour - which makes up the majority of Bangladesh's overseas workforce. For example, in Singapore, authorities recently increased the levy on such workers. If these measures were to pick up across Asia, then there could be a small risk to Bangladesh' remittances. However, with the MENA region remaining the dominant source of flows, we think the picture will stay healthy for the time being.

Trade improving on oil and food

The other major component of the current account is the trade balance. While this remains in deficit - largely due to weak demand from Europe and the US, and a large oil import bill - the net outflows have been in decline in the past few months. This improvement has been largely due to weaker imports, though exports have also picked up, particularly in textiles.

The central bank highlights the import slowdown in food grain and consumer goods as a key driver. This was achieved due to existing high food stocks and good domestic harvests, along with lower oil imports during the first half of FY 2013. While the food picture looks set to keep imports low for the time being, there is a risk that the deficit widens again this year.

One risk factor for the trade deficit comes from the exposure to the Eurozone and the US, which account for almost 67 percent of Bangladesh's exports. With growth in these markets likely to remain subdued, demand for Bangladesh's key exports could be weak. To mitigate the risk of export over-concentration, Bangladesh has started to diversify its exports across Asia and EM gradually.

However, the majority of the exposure remains to the developed markets, so weak growth there remains a concern. However, our overall view is that growth in remittances will outweigh a slightly wider trade deficit; therefore, we expect the upward pressure on the currency to continue, given the trend in remittances growth in particular.

Forex reserves likely to rise

While these supportive factors should see the BDT continue to rise, we think that FX policy will be an important factor to consider. Like most of its Asian peers, Bangladesh Bank (BB) has been active in building up its reserves to stem recent BDT strength.

BB bought more than USD3.5bn between July 2012 and February 2013. Reserves currently stand at around USD13billion.

According to BB, the buying of USD was aimed at protecting the interest of the exporters (textile and apparel in particular) and migrant workers. It also said such intervention would continue in line with market requirements.

This, in our view, will keep BDT appreciation relatively modest. While sterilizing such intervention does entail some costs (BB pays 5.25 percent on its reverse repos to absorb liquidity from the domestic market) at this stage it seems that BB is willing continue to build reserves, slow currency appreciation and support exports.

Capital account risks and opportunities

The capital account is historically small compared to the current account, in part due to the fact that financial infrastructure in Bangladesh is still developing. As such, capital inflows have a smaller impact on the BDT.

However, in 2011 one reason for the sharp weakness seen in the BDT was capital outflows, and as such we need to remain vigilant against such flows reoccurring. The main driver of the negative current account has been the "other investment" component.

Historically, within this, trade credits have recorded huge outflows. The dependence of Bangladesh on trade credits to service its import needs is still a concern. However, should imports continue to narrow as outlined earlier, we think that the need for trade credits should also narrow.

Another component that is slowly picking up is FDI. Net FDI inflows into Bangladesh have been quite modest, both in comparison with regional standards as well as total foreign currency inflows. However, improving macroeconomic fundamentals and foreign interest in tapping new markets have seen a rise in FDI flows.

Within this, the key areas for investment have been services, agriculture, engineering and clothing sectors. If Bangladesh continues to invest in its physical infrastructure this should bolster investor confidence and ensure further inflows.

External borrowing not a major issue

Bangladesh has also been a major recipient of foreign aid in recent years. The IMF recently disbursed a US$140m loan, the second instalment from the Extended Credit Facility Agreement, which was approved last year. Further disbursements will be pending ongoing policy effectiveness and macroeconomic management.

The IMF notes that "recent easing, while modest, should proceed further only when macroeconomic and financial stability is firmly established". Should BB retain a relatively more hawkish stance then this should be another stabilizing factor for the BDT.

More broadly though, the trend for foreign borrowing has been on a decline. Bangladesh's net external debt has been following a downward trajectory, suggesting a low risk of external debt distress.

Furthermore, most of the external debt in Bangladesh is mostly of medium-and long-term nature. This suggests there is little chance of acute pressure rising on the BDT from a pick-up in debt-servicing.

BBN/SSR/AD-17Mar13-12:40 pm (BST)