Washington, DC (BBN) - The World Bank (WB) is lowering its 2015 forecast for crude oil prices from $57 per barrel in its July report to $52 per barrel.

The revised forecast reflects a further slowing in global economic performance, high current oil inventories, and expectations that Iranian oil exports will rise after the lifting of international sanctions, according to the WB’s new Commodity Markets Outlook, a quarterly update on the state of the international commodity markets.

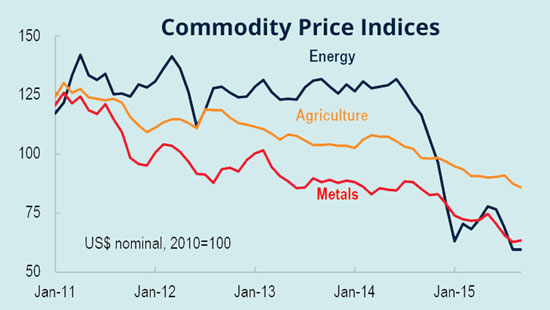

The WB’s Energy Price Index tumbled 17 per cent in the third quarter of 2015 from the previous three-month period, led by a renewed plunge in oil prices prompted by expectations of slower global growth, particularly in China and other emerging markets, abundant supplies, and prospects of higher Iranian exports next year.

Energy prices are expected to average 43 per cent lower in 2015 than in 2014. For commodities excluding energy, the World Bank reports a 5.0 per cent decline in prices in Q3, and forecasts that non-energy prices will register a 14 percent decline in 2015 from the previous year’s levels, according to its latest update.

“We see a five-year-long slide in most commodity prices continuing in the third quarter of 2015. There are sufficient inventories of oil and other commodities and demand is weak, especially for industrial commodities, which is why prices may stay persistently low,” said John Baffes, Senior Economist and lead author of Commodity Markets Outlook.

Impact of El Niño on commodity markets

Despite expectations of one of the strongest El Niño episodes on record, the weather pattern, which affects winds and water temperatures of the Pacific Ocean and changes precipitation levels, especially in the Southern Hemisphere, is unlikely to cause a spike in global agricultural prices because of ample supplies of most agricultural commodities and weak links between global and domestic prices.

This is consistent with the limited impact on global markets of past El Niño episodes. To date, global agricultural prices have declined while those of key domestic markets have not shown large deviations from trends due to El Niño.

However, El Niño could be a source of significant local disruptions in the most affected regions, the Outlook says. In particular, the weather pattern is likely to have a greater impact on more isolated local food markets, which are not linked to international markets.

Possible effects of the Iran Nuclear Agreement on global energy markets.

Within several months, Iran could increase crude oil production by 0.5-0.7 million barrels per day (mb/d), potentially reaching a 2011 pre-sanctions level of 3.6 mb/d. In addition, Iran could immediately begin exporting from its 40 million barrels of floating storage of oil.

Given that Iran has the largest known gas global reserves (18 per cent of the world total), it has the potential to produce and export a significant volume of natural gas over the long term.

“The potential impact of Iranian oil and gas exports on global and regional markets could be large over the long term if Iran can attract the necessary foreign investment and technology to leverage its substantial reserves,” said Ayhan Kose, Director of the World Bank’s Development Prospects Group.

Uncertainty about Iran’s capacity to ramp up exports adds to risks to the energy-price forecast. Downside risks include higher-than-expected OPEC production and continuing falling costs along with improved productivity of the U.S. shale oil industry.

Slowing demand and high stocks could further weigh on oil prices. Upside risks include: an accelerating decline in U.S. shale oil output, and reduced supply because of geopolitical events.

The Outlook provides detailed market analysis for major commodities groups, including energy, metals, agriculture, precious metals, and fertilizers.

According to the report: Metals prices fell 12 percent in Q3, the fourth consecutive quarterly decline, reflecting slowing demand, notably from China. The WB projects metals prices to fall by 16 percent in 2015.

Precious metals prices fell 7.0 per cent in Q3 and are likely to slide another 8.0 per cent in 2015 on lower investment demand.

Agricultural commodity prices fell by more than 2.0 per cent in the quarter and are likely to fall by 13 per cent in 2015, reflecting abundant supplies and high levels of existing grain stocks.

Fertilizer prices fell 1.0 per cent in Q3, and may decline by 1.0 per cent in 2015, because of weak demand, and rising supply.

BBN/SSR/AD